11 tax-free income in India – every investor should know

Paying Income tax is one thing, which most of the people do not like. Everyone tries to minimize their income tax y some or the other means. So today, I will be sharing with you list of some income’s which are 100% tax-free in your hand.

Yes – you heard it right. if you earn these income’s, then you do not pay any income tax on them at all. This article is mainly for information purpose, because I have seen many investors who are yet not clear on the taxation rules of few income’s. Here we go

1. Interst on saving bank interest – upto Rs 10,000 a year

From 2013 onwards, a new section 80TTA is introduced under which, the interest on your saving bank account upto Rs 10,000 is not taxable. So if your saving bank interest for a year is Rs 20,000 . Then out of that Rs 10,000 is exempted and only the rest Rs 10,000 will be added to your taxable income.

This is a great relief for tax payers, because it was really a big headache to find out the saving bank interest from all the accounts and add them up and pay income tax, because for most of the people, it would be few hundreds or thousands of interest income. Now that is gone !

2. Interest earned in NRE account

Any interest you earn on your NRE account is 100% Tax-free in India. Here we are talking about both, the Fixed Deposit and normal saving bank interst. Both of them are tax free for NRI. NRE deposists are a great way to earn a decent interest on the savings done by NRI. Some of our clients even go an extent of taking loan from the country they are working in like UAE/Singapore because they get it at 2-3% and then reinvest the same in NRE deposits here in India where they earn around 8-9%. Also because there is no tax, hence TDS is also not applicable to the NRE account deposits.

And the best part is that the money in NRE accounts is repatriable, means if you are in US and you invest some money in India in your NRE account, the principle and interest money can be taken back to US .

3. Share of Profits paid to partners in firm

If a partnership firm earns some profit and instead of retaining it within the partnership firm, its paid to the partners as a share of profits, then its tax free in the hands of the partner, because the tax is already paid by the firm on it.

So is A and B are partners in a firm, and they get 5 lacs each in a year as the share in the profits earned by the firm, then it will be tax-free in their hands. Note that if they are receiving any salary from the firm, then its taxed in their hands only.

I would like to request that as this is related to corporate tax, please consult a qualified CA on this issue.

4. Maturity or Claim amount received by Life Insurance Company

The money you get from life insurance companies on maturity, claim or surrender is 100% tax-free provided,the premium paid did not exceed 20% of the sum assured. I am quoting new amendments which have come in recent years

As per amendments introduced in the Finance Act, 2003, (i.e., with effect from April 1, 2003), any proceeds received on account of maturity/surrender of an insurance policy were exempt from tax only if the premium paid did not exceed 20% of the sum assured. As an example, if the annual premium is R10,000, to qualify for exemption, the minimum sum assured under the policy was required to be R50,000.

If the sum assured was less than the said value, the entire maturity proceeds would be taxable. Such limit of 20% was later reduced to 10% by the Finance Act, 2012, (i.e., with effect from April 1, 2012) to increase the insurance coverage amount, i.e., the sum assured threshold was increased from a minimum of five times of annual premium to 10 times. For policies taken on the life of a disabled person or person suffering from certain ailments, the limit was relaxed to 15% of the sum assured with effect from April 1, 2013.

5. LTA money received from Employer

Most of the companies pay LTA each year to their employees, which can be utilized for traveling purpose. This LTA is not taxable in hands of the investor provided they provide the proof of travel. So if your company is not paying you any LTA, ask them to restructure your salary and label some part as LTA, because almost everyone spends a minimum amount traveling in a year.

For example, if you are getting a salary of Rs 5 lacs and their is no LTA in your salary component, you can ask your employer to label 20k as LTA and rest 4.8 lacs as other components, this way you will be able to save tax on that 20k part at least.

6. Money got under VRS scheme upto Rs 5 lacs

If a person takes VRS (Voluntary retirement scheme) than any amount received up to Rs 5 lacs is income tax-free. However, not everyone is eligible for it. Only employees of Public sector companies or an authority established under a Central or State govt is eligible for this.

7. Money received from your EPF account after 5 yrs

The money one gets from their EPF account is also tax-free, provided the money is taken out after 5 yrs of service. A lot of times investors change their jobs in 3-4 yrs and withdraw their EPF money only to realise that they could have timed their withdraw in better manner and save 30% of their EPF money which went into income tax (assuming they are in 30% tax bracket).

8. Profits from shares or equity mutual funds after a year

When you earn any profits from your shares or equity mutual funds after holding it for minimum 1 yrs, its called Long term Capital gains, and its 100% tax exempt as per current tax rules.

For example, if you invest Rs 1 lac in shares and after 2 yrs its worth is now Rs 2 lacs. In this case when you sell your shares, you will not be paying any income tax on this Rs 1 lac profit because of long term capital gains rules.

However, it’s important to know that exemption is allowed only when Security Transaction Tax (STT) has been paid (which is paid by you when you buy on recognised stock exchange such as BSE or NSE). But if you do a out of exchange sales, then STT might not get paid and hence in future when you sell shares, you will have to pay tax on profits.

9. Dividends received from your shares or equity mutual funds

You receive dividends from your stocks or equity mutual funds (dividend option). That dividend money you get is also tax-free in your hand. However, the bad side of the story is that company anyways pays the dividend distribution tax to govt before giving the dividends to its shareholders. Hence, anyways we are getting slightly less share of profits in our hand anyways.

10. Amount received by way of gift on marriage

Any amount you get as gift on your marriage is tax free. So your friends, relatives or any random person can gift you any amount or something valuable as a gift on your marriage, and it will be non-taxable for you. Just make sure that the timing is matched with your marriage and the gift date. It should not happen that you get some gift after 2 yrs of marriage and you try to justify that it was a gift for your marriage.

Its like this, If you are getting a gift of Rs 10 lacs from a friend (which is nearly impossible), ask them to hold on for a while and gift it to you after few months or a year when your wedding is in place and you will save a lot of taxation issues

11. Any amount received through WILL or Inheritance

There is no inheritance tax in India now. So any-thing you get in inheritance through WILL is not taxable in your hands. It becomes your property and now when you invest that money, only the interest part earned on that property will be taxed.

And Many more

Note that, it’s not possible to list down each and every income which is tax-free. Here I have listed 10 income’s which I think most of the investors should be aware about this. There are many other things which are not taxable, but it applies to certain section of investors.

The dark side of becoming an Entrepreneur – 5 things no one will tell you on face

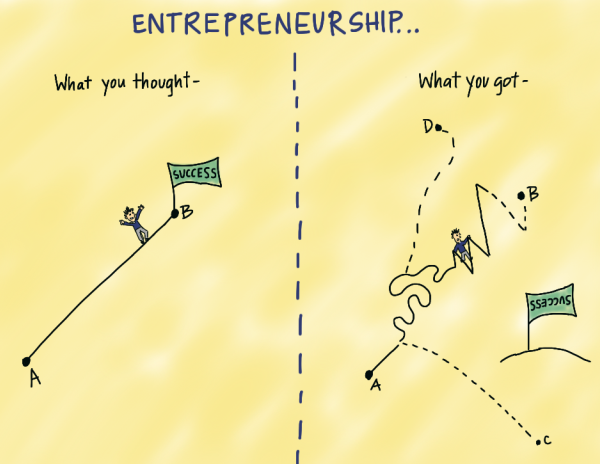

Have you ever dreamt of leaving your job and starting something on your own? Are you frustrated in your job and don’t see a future? If that’s the case, I am sure that, you must be excited by the thought of “being your own boss” someday. Hence, do read this article fully before you take any final decision.

Last year, when I wrote my own story of how I had quit my job and went full time working on this website, I saw that a lot of people were impressed with my story. Everyone said it was a brave decision. A lot of people could relate to my situation and said that even they are looking forward to quit their jobs sometime in future and jump into entrepreneurship.

Pursuing your passion and getting out of your boring corporate job is definitely an amazing experience. It gives you a great satisfaction, sense of achievement and can be extremely rewarding, but only if things go right.

But WAIT .. you know what !!

You probably don’t have much idea of the other side, the darker side and thats what I want you to read in this article.

“Pursuing your passion” is over-hyped

Yes, you heard it right!

I have realized that the positive side of entrepreneurship is often over-hyped. Surely there are many awesome things of being your own boss, but then there are challenges and issues involved, which are buried deep down in the entrepreneurship world, not openly shared or communicated in detail.

When you meet a young entrepreneur who left his well-paying job to pursue his passion, what do you see in his life? I am sure you must be seeing the freedom he has in his life, the exponential growth prospects, no boss to report to and the satisfaction on his face. Right ?

But you never see the problems, issues, challenges and frustration which arises out of being an entrepreneur. I know it very ‘cool’ to leave your job to pursue passion and it has created such a glorious image in the eyes of people, that majority of them want to try it out someday in their life. But remember the old saying …

“The grass looks more, greener on the other side”

5 side-effects of being an entrepreneur

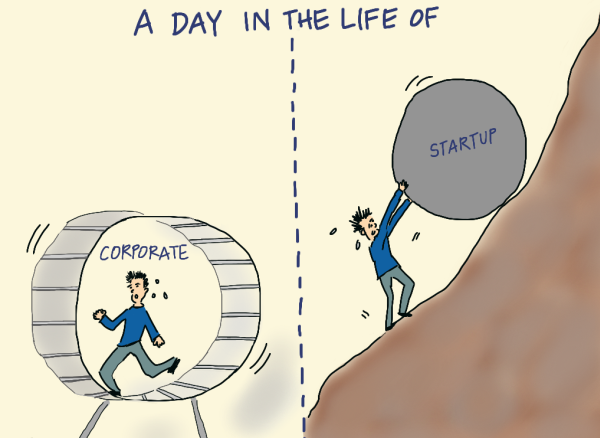

I know how amazing it feels when you leave your job to pursue your dream. It’s an awesome feeling. I have done that and been there myself. There is growth prospects, freedom and sense of satisfaction and many other great points. But today we are not going to focus on that because you already know all that. Today, I want to share the darker side. I want to share the challenges and problems which a person faces in his entrepreneurial journey.

I have also contacted few business owners and asked them for their experience and real-life issues they are facing, which you will read below. It would be a great thing to be aware of these challenges, so that in future you can take an informed decision on what to do and which side you should move. So here we go ..

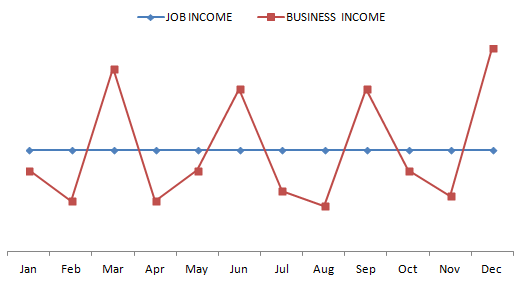

#1 – Be ready with the inconsistent income

The worst nightmare for a salaried person can be an unknown number getting credited in your account every month. When you are into a job, you get a number deposited in your account each month, not less not more. You know the date, you know the amount and you are clear that its going to come for sure.

Things like rent, EMI, household expenses, bills and many other things are already defined and dependent on your salary and for most of the people, they just can’t afford any cut in their salary because their monthly structure will fall like a pack of cards

When you are into your own work, a big problem is a variable income and this is more true in the starting years. Sometimes you get Rs 40,000 in a month and another month, it can be Rs 1 lac or nothing. Over time, this uncertainty goes down, as your work improves and your foundation gets strong. You slowly move to a more consistent income zone, but still the variability remains in the income.

A real life Experience

Amit Singh, who runs an IT company in Pune shared his real life experience of how he faced cash crunch at one point of time and how he felt about it

You will run out of money and unless you can handle the stress that will follow, you should not attempt to be an entrepreneur.

I will tell you my experience, in the initial days everything was as I had imagined, but then came a time when we had no projects for more then two months we run out of all our saved money, during that time the team I was counting on failed me, we had a very hard and stressful time, but it was ultimately my responsibility and blaming would not have solved the problem.

It took us six months to recover from that two months financial liabilities.

For most of us it’s long working hours and no holidays, for a long time you will not be able to take any vacation and you will be working for average 12-14 hours every day. You should also forget about work life balance, it will only be work.

#2 – You will doubt your decision many times

While a job has its own frustration, working on some venture also comes with its own set of psychological problems. You always wonder if you made the right decision or not, especially if your income is not as per your expectation or if you come across some challenge and that affects your business, you get many sleepless nights wondering if you took the right decision or not.

One of our readers, Rishikesh Sinha shared what he thinks about this point and he shared his thoughts and experience.

Sometimes when I feel low and analyse things around me in terms of monetary and relationships with people, including near and dear ones. I find, entrepreneurship is indeed tough and demanding. I don’t have enough money for disposal, to spend on things that brings happiness or comfort, though momentary it may be. Had I been an employee, atleast I could very well spend on necessary things without blinking an eyelid. But it is not in case of being an entrepreneur, a rupee spend has to be weighed upon. It seems the money I earn is not mine, it is of the customers.

This is about money. In case of relationships even, you find money plays a pivotal role. Being a brother, being a son, being a neighbour, being a husband, being a friend even, my monetary role — someway or other way — plays its role. And I find it hard to comply with all these roles. I see around, being an employee people have done what they could do the best with themselves. They are happy with no remorse.

Here I find, had I been an employee atleast I could have kept many people happy (if not all) in terms of monetary. People would have looked at me as a successful and resourceful person. But in case of entrepreneurship, since they don’t see money coming out of my pocket, my existence doesn’t count.

One more benefit, that I see being an employee is that he or she becomes the extension of the organisation. This is a great benefit as a person. You are being defined with your organisation. In case of entrepreneurship, it is not the case. You and your business are alone. You are always vulnerable to predators.

If one month goes bad, you start feeling tremors under your feet and it’s really very disturbing fact, because then you extrapolate that one bad month into distant future, and start thinking – “What if the whole year goes like this?”. Your imagination takes you to extreme possibilities and you are devastated. Job has its own challenges and doing your own work also brings its own set of challenges. The image below depicts it quite well.

Only after this has happened to you many times you overcome this feeling and stay relaxed.

#3 – Lack of focus in work

This point is one of my favorite. When I left job, I always thought that now, I am going to be my own boss, no one to disturb me and no one to questions me. I will focus all my energy and time in things which I love.

I was delighted and thought – “WOW – No one to monitor, no deadlines and no one to report to”

What an amazing situation it would be.

However, now after almost 4 yrs, I can assure you that my thinking was wrong. What seemed like a blessing turned out to be a curse. Because there was no one to monitor, and because there were no deadlines, things didn’t happen on time and the productivity went down. I didn’t report to someone, hence there was no one to push me to do things on time, I was my own boss and I always forgave myself for everything wrong I did.

When you are in job, you have a deadline, you have someone above you who will demand things and you are forced to focus on your work. But when you are on your own, its a big challenge to do things on time. The freedom comes at a big cost. I can start my work at 2 in afternoon and unless I have a great discipline, it affects my business. The above points are more true, if you have a home office kind of setup.

When you don’t have a boss or company tracking your progress, it’s easy to lose focus. Your freedom to do whatever you decide with your time will backfire if you don’t stick to a schedule and plan. Today, things like social media notifications can lead you down time-wasting rabbit holes.

So understand that when you are not into job, its really really tough to follow a 9-5 kind of schedule because it doesn’t exist at all and sometimes you wonder, if a strict timeline and someone yelling on you to be late was a blessing in disguise.

#4 – You can still be frustrated

It’s very much possible that in reality your plans might not workout as per your expectations. You had high energy and motivation when you begin, but then somewhere in between things start settling down and after a while, your whole excitement fizzles away and you get frustrated at your work and different things you have to deal with in life.

Hence, it’s very important that you carefully choose why you want to leave your job and start something on your own. Just because you hate your current job, can’t be a strong reason to quit. I suggest you to find a more stronger reason to quit, because boredom and frustration are part of any kind of work especially if you are not innovating after few years and you get into that cycle again.

A lot of people say “I hate my job” . But that alone cant be always a reason to follow your passion. Here is a comment made by a reader on this topic

But before quitting job just make sure that you are leaving your job because you reallyy passionate abt what you REALLY want to do or start. You simply love it..

It absolutely does not make sense that I hate my current job and that’s why I want to quit it. Always think why you hate your job. It’s because you lack somewhere or you are not having proper skill to do it otherwise you like your job. If that’s the case start working on areas where you are lacking (Comm skills, technical skills etc..)

I am also in Software field and in future my plan is to go in Education field because i think i can really make a difference there but before that i would like to make sure that i am really passionate abt it and i am working on it..

Just because you hate your current job, does not qualify as the reason for doing some business on your own because if your heart is not in that, you will again start hating it. One of my friend Nooresh Merani (appears on CNBC) does exactly that. He left his IT job to become a full time stock trader, not because he hated his job, but because he loved trading 🙂 . Below is his story in his own words ..

The biggest reason for an entrepreneur to become one is to love some work/hobby/ passion for which one is ready to make a lot of sacrifices.

So when i quit an IT job it was the love for being an advisor, trainer , trader and not because i hated my job. Well i loved the 6 months in that job as i was on bench and getting paid for having fun and also run the blog. The worst way to become an entrepreneur is to hate ur prev job.

A lot of entrepreneurs will talk about how when there is no revenue no income and working so much for it was a dark period. It makes all of us feel good as we have taken the other road. There is a tough part when you are doing good business , good income you have to make many more sacrifices as you are a boss 24/7 and not an employee 9-5.

So for example 2007 was equally tough for me in hindsight. As very rarely met my friends, sports reduced , had free tickets to ipl from friends ( he even took his barber ) and i could not make it for even one of the matches. Work was 24/7. Luckily i was single :).

Learnt from that and had a lot of fun in a lean period post 2008 where markets were sideways 😉 . An entrepreneur needs a support staff in his/her family as the toll comes on them for the sacrifices. Entrepreneurship is like another marriage where your wife ( if u have one ) ur mom/dad and friends accept your second wife.

For them to change , sacrifice is tougher.

One standard example – every entrepreneur needs capital/ raw material which can be intellectual, hard cash or money , technology. Also capital requirements are needed to for further growth. What you do not have ? Are you ready to stay on rent ? Are you ready to mortgage property ? Many tough questions.

You will not even get a home loan 🙂 or a car loan easily. I could stay on rent for 8 yrs because of support from parents and then my wife and in laws 🙂 i still do for comfort but have an own flat too.

I always remember these lines even if i plan to work for someone or myself. The monthly salary is one of the most harmful addictions and the only one which lets you live and not kill.

Nooresh has also done a nice presentation for those who love stock markets and wondering how to become a full time trader

#5 – Your work and life balance goes for a toss

When you get into your own work, the one big issue is that your work and life generally becomes one. Because now you are the boss. You sometimes work from home, you go to office sometimes, you might have few things to work on Sunday’s , early morning and round the clock few times.

The hardest part of being an entrepreneur is to draw a line between work and personal life. Especially those who started their journey before marriage, they will find it hard to balance the two life. Undoubtedly finding that balance is essential, as soon your personal life will start governing your professional life. Leaving the zone of being workaholic is not going to be an easy task, and here is one quote to help – “Family happiness is the ultimate reward for my hard work”

Success comes with a cost, and sometimes it’s too high. If your friends share the same vision or share the same bandwidth as yours, you will have no problem. If not, get ready to walk alone. Your friends will be supportive, will appreciate your work, but they won’t be there when you need to discuss an important idea or problem. Moreover, success begat loneliness, and when you move ahead in life, it would be harder to have new good friends.

The liberty of leaving your work as it is on friday evening, only to resume it back on monday morning is absent most of the times. You personal life gets affected due to this, because your family wants a separate time from you and they might find it frustrating that you are never completely out of your work.

Should you leave your job, even if you are earning a good enough salary ?

Given the kind of salaries some people are making these days, many a times I feel that one should work for few years even if they are not in love of their job and make some decent money and reach a milestone in their lives before plunging into entrepreneurship.

This is more true for sectors like Software, because I have seen some people making amazing salaries which is just not possible in first few years of struggle when you work on your own and given how important money has become in these times, I think its makes more sense (not always, but in most of the cases) to give some time with focus on making money only and acquire basic things in life first before you plunge to take risk

Example

One of our clients has just returned from Australia and is around 38 yrs old. He has been making good money from many years, and wanted to open his own restaurant in Pune and this thought was in his mind from the time he started working at age of 27. But the salary was too good to ignore. So he decided that for 10 yrs, he will focus all his energy into making money only and reach a milestone first. Today he has a flat with no EMI, a respectable bank balance and now he thinks, that it’s a better time to take the decision of leaving his job to pursue what he wants.

So if in your case, you need to decide if it makes sense to work a little more years only for the reason of making some more money and reach a situation which will allow you to take the decision of quitting you job more easily. Only you can decide that.

Entrepreneurship can be a very lonely world

I asked Ronak Hindhocha, one of my professional friends to share this views on this topic and what has been his experience and below is what he says

Entrepreneurship is a very lonely world unless you have a co-founder who totally understands your business. If not, it can be very difficult to build a team that can match up to a level where they start knowing what you go through day in and day out.

A lot of times, you’d feel like quitting. You can quit from inside but you can’t show it to the world. With each passing failure (whether big or small) things only get tough. To a point where you start questioning whether you’ve made the correct decision by venturing into the unknown.

For entrepreneurs who are in a product business (which works very differently than a service business) it can be extremely painful especially for first time entrepreneurs. You come across so many unknowns and if you are lucky enough to survive the first 2-3 years you almost get used to the daily grind.

Entrepreneurship takes a toll on your personal life. And yet, you cannot survive without their active support. So, you’ve got to try really hard balancing personal and professional life. It forces you to bring down your standard of living many notches down. While earlier you’d not think twice before going for a movie or spontaneous shopping spree you’d now find yourself defending why those unnecessary splurges no longer make sense.

Entrepreneurship makes you anti-social over period. You no longer enjoy social gatherings where pointless discussions are a norm. So there comes a point where you stop attending them. Your family/friends start wondering if you really care about them. Sure, you’ll piss of some of them. The true friends will remain but lots of them will stop worrying/caring about you. And the anti-social animal within you won’t care either.

You should also view this video below from Nadia Arain, where she talks about the Dark Side Of Entrepreneurship and her experience.

Having skills does not mean everything

Job and business needs different skills, mindset and dedication. Some people are not born to be employees and some are not born to be employers. It’s totally fine to know which side you belong to and accept that fact.

Neil Patel, one of the most famous internet entrepreneur shares his view about what is required for entrepreneur life

Strategic vs Being Negative

I know that to some people, all what I am saying will sound a bit pessimistic. But that’s not the case, I am just trying to say that you could time your decision in a better way and with proper planning, which will increase your chances of your success with a huge margin.

There are many examples, where a person left the job to pursue the passion and it didnt work well and after 2-3 yrs of struggle, they had to come back to their jobs and that too at a lower salary, because their career went back by few years.

For example, imagine that a person with 8 yrs of experience today has a 20 lacs per year package in year 2015. The person has a choice

Leave your job in 2015

Make 1 crore more in next 5 yrs and then leave your job in 2020

There is no right choice here, but only “your choice”. You need to check which option works better for you? It should not happen that in order to chase your dreams, you create a situation where you regret it later and your loved one’s suffer so much, that its beyond repair. Take a responsible decision. Darren Rowse has written a great article on this topic

Doing a job can be equally awesome

I want to just make sure that many people who have started hating their jobs, just understand that there is always some kind of struggle involved even when you are not into jobs. You need to relook at things with different perspective and should appreciate what a job has to offer you. The world needs people who are working in jobs, just like they need entrepreneur. Not everyone can be an entrepreneur and it’s totally fine.

A job, might nor offer the equal exponential growth opportunity like a business, but thats fine. You dont need that always. You should appreciate the consistency of income, good work life balance and an atmosphere where you can grow well in life.

I still miss those days in my past company, where we had team outings, working with colleagues which was kind of another family, going to cafeteria to just waste time with my group (not my team), those free lunches and a complete two days of no work. You can always pursue your dream on the side slowly transforming it into a stronger part of your career and also create an income out of it. Take some inspiration from this example if you want to understand more on what I am saying.

Atal Pension Yojana – Features & Eligibility explained in detail

Recently the govt has announced the pension scheme called “Atal Pension Yojana”, which is targeted at workers from lower class who work in unorganised sector which constitutes around 88% of the workforce.

An account needs to be opened under this scheme and monthly contributions needs to be made till the time of retirement after which a pension amount ranging from Rs 1,000 to Rs 5,000 per month would be paid to the account holder and on death of subscriber and spouse, the nominee will get the lump sum accumulated by the end of the period. Any person below 40 yrs can open an account.

The retirement age will be set to 60 yrs, hence one will get at least 2o yrs of contribution. Any person below 40 yrs can open an account. The retirement age will be set to 60 yrs, hence one will get at least 2o yrs of contribution.

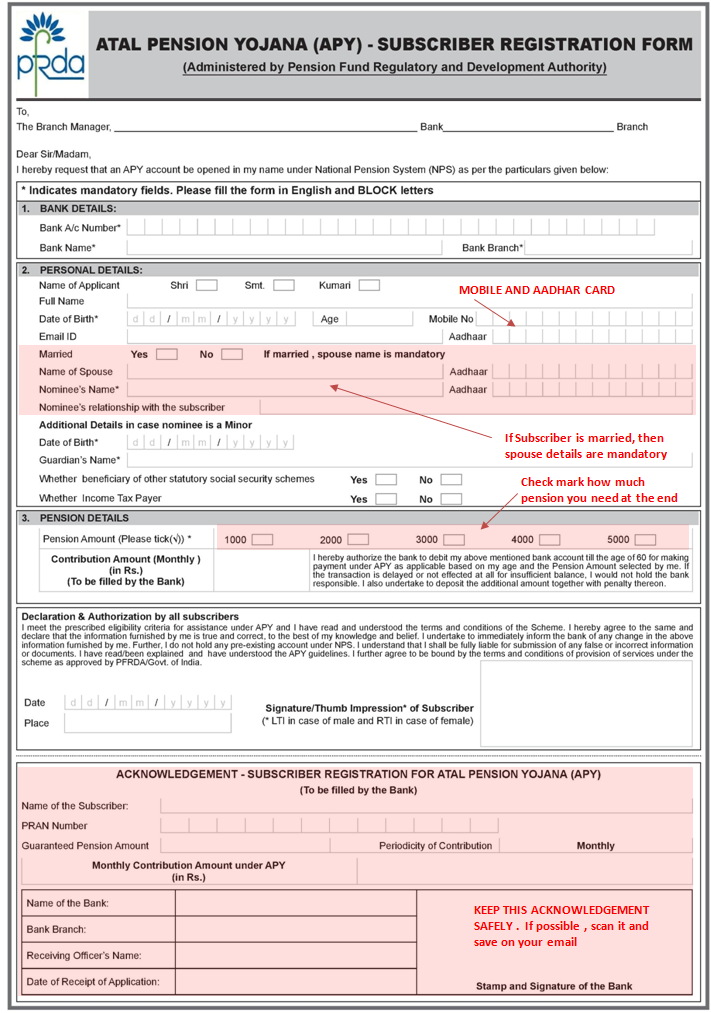

How to open Atal Pension Yojna Account?

Go to the bank where you have your saving bank account like SBI, ICICI, HDFC or any other bank..

Mobile number is compulsory, hence that needs to be filled

If you have aadhar card, provide the number in the form (but its not compulsory)

You also need to provide spouse details if applicable and nominee details, which is compulsory

You will select the pension amount you need in future and based on that the bank official will write the monthly contribution required on the form

Below is a sample form

Note that the form itself contains a section which mentions that you are authorising the bank to deduct the monthly contribution from your account till the age of 60 yrs. So once the account is opened, your account will then get auto debited in future every month. If one does not have a bank account, then one can give their KYC documents along with account opening form with the Atal pension Yojna account form.

Eligibility Criteria for Opening an account

The age of the subscriber should be between 18 – 40 years.

One should have a saving bank account or should open a new saving bank account

One should be having a mobile number, which needs to be furnished at the time of filling up the form

Government co-contribution for 5 yrs

If one joins this scheme between 1st June, 2015 to 31st December, 2015 , the govt will co-contribute 50% of the total contribution or Rs. 1,000/- per annum, whichever is lower for the 5 yrs period from 2015-16 to 2019-20 , But this govt contribution will be available only for those who are not covered by any Statutory Social Security Schemes and are not income tax payers. What that means if that if you are an EPF subscriber, then you will not be eligible for govt co-contribution part.

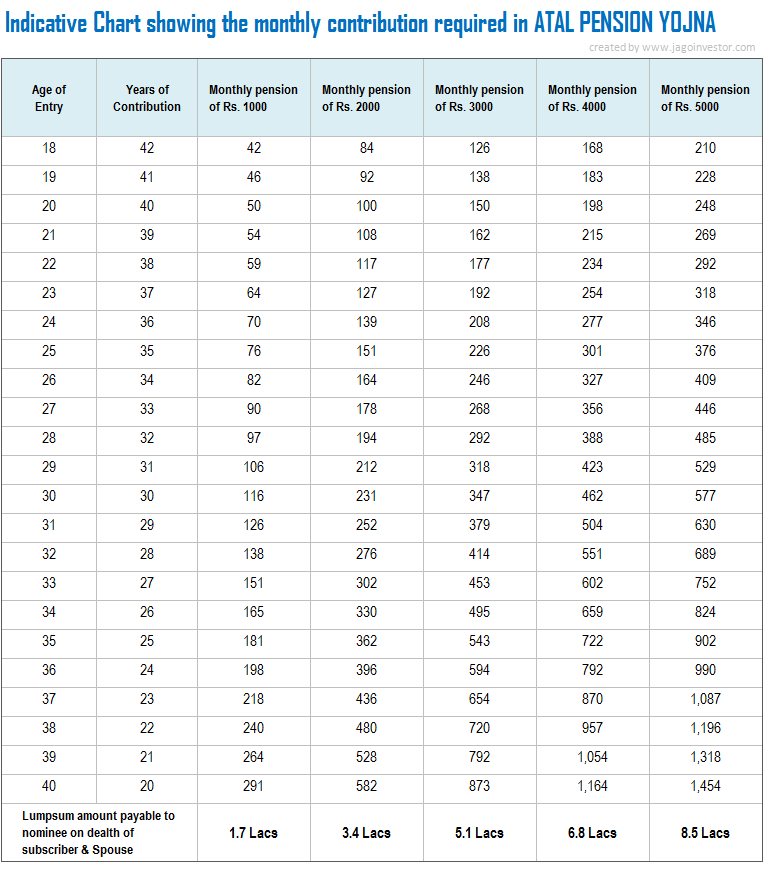

Below is the indicative monthly contribution required in this scheme at various age limits.

The subscriber can increase or decrease their contribution amount at some later stage if they want to do it

Will you get statements of transactions?

Yes, you will be getting regular intimations on your account information through SMS and even a physical statements each month. Note that you can move to any part of India without interrupting your contributions because the deductions will happen automatically from your bank account.

Can you exit or partially withdraw from the scheme ?

1. On attaining the age of 60 years – The first option is when you reach 60 yrs of age. At that time you will be able to use 100% of the money, but only in the pension form. You will only get the pension per month and not the lumpsum amount.

2. In case of death of the Subscriber (once they cross 60 yrs) – In case of death of subscriber, pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus would be returned to his nominee.

3. Exit Before the age of 60 Years – The Exit before age 60 yrs, would be permitted only in exceptional circumstances, i.e., in the event of the death of beneficiary or terminal disease. As per wikipedia, Terminal illness is a disease that cannot be cured or adequately treated and that is reasonably expected to result in the death of the patient within a short period of time. This term is more commonly used for progressive diseases such as cancer or advanced heart disease than for trauma.

What is your want to discontinue the payments or delay in payments ?

Non-maintenance of required balance in the savings bank account for contribution on the specified date will be considered as default. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Re 1 per month to Rs 10/- per month as shown below

i. Re. 1 per month for contribution upto Rs. 100 per month.

ii. Re. 2 per month for contribution upto Rs. 101 to 500/- per month.

iii. Re 5 per month for contribution between Rs 501/- to 1000/- per month.

iv. Rs 10 per month for contribution beyond Rs 1001/- per month.

Discontinuation of payments of contribution amount shall lead to following

After 6 months account will be frozen.

After 12 months account will be deactivated.

After 24 months account will be closed.

Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount. The fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

Are there any Tax benefits in Atal Pension Yojna scheme ?

No , there are no tax benefits available in this scheme. A lot of people might think that they will get any exemption under 80C or on maturity, but no benefits are available. The pension amount will be considered as the income for the person and will be added in the taxable amount.

What if someone is already a subscriber of Swavalamban Yojana under NPS ?

All the registered subscribers under Swavalamban Yojana aged between 18-40 yrs will be automatically migrated to APY with an option to opt out. However, the benefit of five years of Government Co-contribution under APY would be available only to the extent availed by the Swavalamban subscriber already.

This would imply that if, as a Swavalamban beneficiary, he has received the benefit of government Co-Contribution of 1 year, then the Government co-contribution under APY would be available only for 4 years and so on. Existing Swavalamban beneficiaries opting out from the proposed APY will be given Government co-contribution till 2016-17, if eligible, and the NPS Swavalamban continued till such people attain the age of exit under that scheme.

Note that, the ultimately the money under this scheme will be managed through NPS only and thats the underlying thing. All the investments decision will happen as per the guidelines of PFRDA.

A good support system for Poor

As I mentioned, this scheme has the maximum pension of Rs 5,000 per month, that too when the person reaches 60 yrs of age, that too will happen only after a minimum of 20 yrs from now (only people below 40 yrs of age can open an account), so Rs 5,000 at that time would be a very miniscule amount. However note that we are talking about the people in lower section’s who are really poor. At least this Rs 5,000 per month would be a great support in their old age when they won’t be working. A subscriber can open only one APY account.

With this scheme, people will be encouraged to save a small portion each month ranging from Rs 40 to Rs 210 per month. Below is the full chart showing how much money would be required to be deposited each month depending on the time of entry in the scheme and the pension amount chosen.

What is the returns of this scheme and should you invest?

So the question finally is, how good is this scheme and its returns if you consider the returns? I did a XIRR analysis of the scheme considering a 40 yrs old person is investing Rs 1,454 per month for 20 yrs , and then gets a pension of Rs 5,000 all this life (till age of 100 years). The returns I get is 7.74% through the excel sheet.

When I do the same thing for a 25 yrs old person invests Rs 376 per month for next 35 yrs (till age 60) and gets pension till he turns 100 yrs . The overall IIR is 7.9% . This includes the lump sum payment at the end to the nominee

So looking at the numbers, we can conclude that the returns from this scheme is in range of 7.5% to 8%. Considering that, Its a guaranteed return from govt of India, I will leave the judgement of its being good or bad to you only.

You should also read, Debasish Basu critical analysis of this scheme on this link to get more understanding about the issues of this scheme.

I would like to again reiterate the point that this scheme is more for the people of poor background who do not have access to any social security scheme already and will be somewhat beneficial for them, and not high-income earners because Rs 5,000 even after 20 yrs will be very very small amount. If one wants to still open this account, one should find a good enough reason for themselves.

Are you investing in this scheme?

I would like to know what you think of this scheme and if you will be opening an account for yourself? You can also suggest this scheme to your maid, driver or any person who you think should get a minimum pension by the time they turn 60 .

5 things to know before you Submit Investment proofs for tax saving

Do you know everything regarding investment proofs which you provide to your employer at the time of tax-saving season? If your answer is NO, then this article will help you understand a lot of things which you don’t know or partially know about. So, I will talk about some of the common things you should take care while giving your investment proofs to your employer for tax saving purpose.

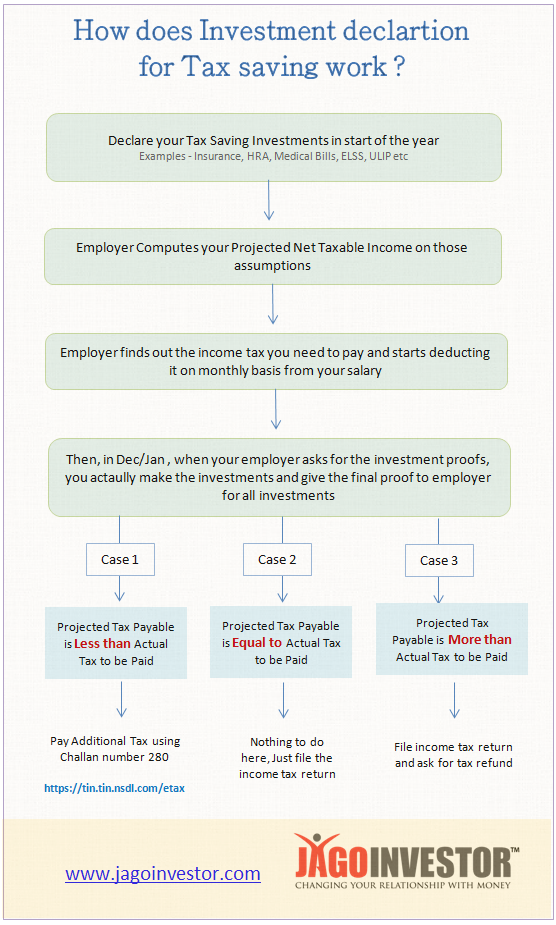

1. Investment declaration helps employer to deduct appropriate tax

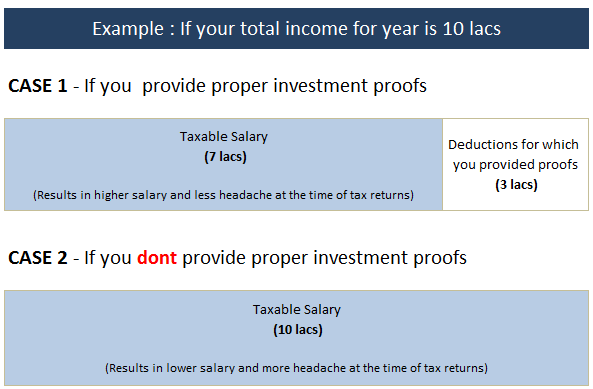

The first and most basic thing you as employee should know that your employer is supposed to deduct your income tax on monthly basis and deposit it with govt on 7th of the following month. For this, the employer should calculate your taxable salary and it can only happen if you before hand give him an idea about how you are planning to save tax, and apart from that how much of HRA, LTA, Medical reimbursements you are entitled for.

For this purpose, your employer asks you to declare your various investments in the start of the year itself, so that they can compute your net taxable salary and then pay your salaries accordingly, after deducting TDS from your salaries.

And then, finally around Dec/Jan, they start asking you to provide them the actual proofs of your investments and receipts so that they can match things with their initial calculations and if there are any difference they have 2-3 months in hand to handle the discrepancies. Below is a small example of it

What If you failed to submit investment proofs

If you failed to submit your investments proofs (you declared them, but didn’t invest in reality), in that case you are liable to pay higher income tax, but employer has not deducted it and hence they get a 2-3 months of extra time to adjust it from your salary. Following things are required by employer as investment proofs.

To claim LTA, you need to provide Travel receipts (flight boarding pass, train tickets)

ELSS investments proofs or any other 80C investments

Life insurance and health insurance premium receipts

Various donations receipts

Rent receipts to claim HRA

2. You can also share your saving bank interest, FD interest with employer

A lot of people do not know this, but you can share your saving bank interest, FD/RD interest earned during year, any capital gains from shares or mutual fund, rental income and other kind of incomes with your employer, so that they get a complete picture of your taxable salary and deduct your income tax which will be more accurate.

If you do not disclose these additional incomes to your employer, in that case – you will have to separately pay additional income tax yourself and then take these things into account while filing your income tax returns.

Note that another advantage of declaring these additional income with employer is that you will not have to pay any penalty which might arise due to not paying advance tax on time.

Also, you won’t have to take the burden of paying the additional tax at the end of the year, the tax will get distributed almost equally throughout the year.

3. Didn’t submit income tax proofs to employer? You can claim things later

A lot of investors have this myth, that if they didn’t do their investment proof submission to employer, they will never be able to claim the deductions and will have to pay higher income tax. This is not true.

Yes, it’s a good practice to give the investments proof to your employer on time, and that will save you a lot of headache later while filing the returns. But for some reason, if you fail to provide the investment proofs (example, like you don’t have money in the month of Jan and you decided to buy a life insurance policy only in Mar), in that case – your employer will deduct the income tax, but then at the time of filing your tax returns you can claim the tax refund, if you finally managed to invest in tax saving products later.

Here is a chart which will give you a better idea

Here is another detailed example of how it happens

Ajay has the salary of 12 lacs a year, and he declares to his employer that he will invest Rs 1.5 lacs in 80C products

Employer based on Ajay declaration will calculate that Ajay taxable salary is 10.5 lacs and will be based on that suppose the total income tax for the year is 60k (just for example) . So Ajay final salary will be 10.5 lacs – 60k = 9.9 lacs. This 9.9 lacs divided by 12 will be 82500 which he will get on monthly basis and the employer will deposit Rs 5,000 as his tax to govt on monthly basis

Now in Jan, when the employer asks Ajay to give them the investment proof, suppose Ajay realizes that he forgot to make the investments and does not have money to invest 1.5 lacs in 80C products. But he will do it in Mar himself. And he fails to provide the income tax proofs to his employer.

Now his employer will come to know that Ajay real taxable salary is 12 lacs and not 10.5 lacs as declared by him and lets say on this his income tax is 1 lac, so additional 40k is to be recovered from Ajay, which will be adjusted from Ajay’s salary in Feb/Mar

Ajay then invests 1.5 lacs in Mar and finally his taxable income should be just 60k , as per the planning (because his taxable income is 10.5 lacs as declared in the start). However his employer has deducted 1 lac in total from his salary and paid to govt.

Now Ajay can declare in his tax returns that he has invested in 80C products and he is liable to get refund of Rs 40,000 which he will get in next few months.

In the example above, you can see that not giving investment proofs on time has resulted in some inconvenience for Ajay, but that does not mean that he will lose out on his tax benefits. One can always invest around the end of the year and then claim back the tax refund later.

However, there is one exemption here

Few exemptions are made only at employer level, like LTA and medical reimbursements. So if you fail to provide LTA and Medical reimbursements proof to your employer on time, then you lose the benefit. You can’t claim it back at the time of filing returns.

4. You DONT need to submit any proofs while filing your tax returns

Another important point you should remember is that while filing income tax returns, you just have to furnish the information about your investments, and not attach any investment proof.

Please do not attach xerox copies at all. It’s not required.

Its required by the employer because they are deducting the TDS and as a third party they need the documents for verification purpose.

But if you are claiming at all the benefits yourself at the end of the year, you just need to declare things. However note that you should keep the receipts and all the required documents with you for some years, because if their is any scrutiny later, you need to be prepared to answer income tax authorities along with documentary evidence.

Which means that you should never lie about your investments which you have not done in reality. Always provide true information.

5. You need to give “proposed investment” proofs for the month of Feb and March

A lot of people are confused on how will they provide the investment proofs for the month of Feb and Mar in Jan itself, when the employer asks for investment proofs. It might happen that your life insurance premium is due in Mar or if you are doing SIP in ELSS funds, you still don’t have the statements showing the investments.

In those cases, you have to provide a declaration that you are going to make the investments for Feb/Mar and based on that declaration, your employer will process the TDS. All the employers provide you with the declaration form. You just need to write there that you promise to do the investments for tax saving in next 2 months and your exemptions should be given to you based on your declaration.

.

.